Taxation methods

The taxes discussed in this guide are all forms of indirect tax. Unlike a direct tax, which is a tax that is paid directly to the government (income tax), indirect tax is collected throughout the supply chain and remitted to the government but is usually included as part of the purchase price of a good or service. Two types of indirect taxes are referred to as consumption taxes. Depending on the country, the two kinds of consumption taxes may be referred to as value-added tax (VAT) or goods and services tax (GST). Indirect and consumption taxes are calculated using a standard percentage that the import country's government determines.

VAT

Most countries use VAT as their main form of taxation. VAT rates, rules, and exceptions are determined at the individual country level. VAT is paid at every stage of a good's production, distribution, and consumption. VAT is charged at every point of sale at which value has been added; from the sale of the raw materials to the final purchase by a consumer. While VAT is collected at each point of sale, a portion of the VAT goes to reimburse the VAT paid by the previous buyer in the chain, and the government gets a portion of the VAT from every stage. Ultimately, the consumer pays the VAT as the last transaction.

Example: A clothing designer would pay VAT on purchased fabric and materials, then later charge VAT on the finished product sold to the consumer. The consumer's VAT payment would reimburse the designer for the VAT paid when purchasing the fabric as well as tax remittance to the government.

GST

GST is another term for VAT in some countries. GST is essentially the same as VAT.

Sales tax

Another kind of indirect tax is the United States (U.S.) sales tax. The U.S. is one of the few countries that does not charge VAT or GST. Instead, the U.S. uses state sales tax as its method of taxation. However, there are several criteria that need to be met in order for the sales tax representative to be able to collect sales tax. While VAT is paid multiple times on a product (at each level of production, distribution, and consumption), sales tax is only charged on the sale of goods to the consumer.

U.S. state sales tax: Sales tax is a one-time tax charged at the point of purchase. The consumer pays sales tax to the retailer, and the retailer then remits it to the government. The end consumer is the only one who pays sales tax. If a manufacturer or retailer purchases something for resale, they are not responsible for paying sales tax on their purchases. Sales tax rates, rules, and exceptions are determined at the local and state level. Retailers don’t have to collect or remit sales tax when selling online from state to state in the U.S. unless they have a business presence in the state (nexus), which is created by having a physical presence (buildings, employees, or salesperson visits) or an economic presence (selling above thresholds determined by each state). Retailers must have a business presence (nexus) or they must sell above a certain value within the state where the buyer is located to collect and remit sales tax in a state where the buyer is located.

Example: A shopper in Utah purchases a shirt online from a store based in California. The retailer has no nexus in Utah; therefore, they do not need to collect sales tax on this order.

U.S. import sales tax: The U.S. does not have a national sales tax applicable to imports. International (and domestic) sellers are only required to collect and remit sales tax when they have nexus in the state they are selling to.

Compare taxation methods

As established above, VAT/GST and sales tax are all forms of indirect tax, meaning that the end consumer ultimately pays the tax. Another similarity is that governments impose these taxes to generate revenue. But how do they compare when it comes to cross-border transactions?

-

Tax is paid at every stage of the product life, from production to sale, where there is an increase.

-

Whomever is buying the raw materials, wholesale goods, or final retail product is required to pay VAT or GST whether during production, distribution, or consumption, with rates being determined by the laws set in each country.

-

Each business must remit the tax collected to the government.

-

- The tax is collected at every stage of production, distribution, and consumption.

-

The tax amount is usually included in the total price of purchase (inclusive).

-

A VAT invoice must be issued within 15 days prior to the end of the month in which the goods or services were supplied.

- Failure to issue the onvoice within the alloted time could result in illegally charging late fees.

-

Depending on the country, VAT and GST are typically reported with the help of a tax authority.

-

For countries with low-value tax schemes, such as the UK, EU, Australia, etc.:

-

Cross-border VAT is usually collected by customs unless it is a low-value shipment.

-

International low-value taxes (ILVT) are self-reported.

-

-

At each level of payment and VAT charge, a portion of the VAT reimburses the VAT that the previous buyer in the chain paid.

-

Reclaimable VAT expenses from tax authorities varies from country to country.

-

Reclaiming taxes is not available for the end consumer.

-

Audits are conducted by the territory's government, and procedures are similar to sales tax.

-

Because VAT/GST can be reclaimed, businesses audit each other and compliance improves.

-

Cross-border VAT is typically collected by customs, although new VAT laws are beginning to change this.

-

New laws are shifting responsibility to sellers/businesses to collect VAT.

-

GST/VAT are self-reported domestically.

-

Cross-border GST/VAT are typically collected by customs.

Tax scenarios

See the flow of how VAT and GST are incurred from manufacturing to the final sale in the examples below.

- Input tax: An input tax is a tax paid upon the purchase of materials or services needed to produce goods or services that you sell as output.

- Output tax: Output tax is a tax that is charged to the customers who buy the output of your production or sale.

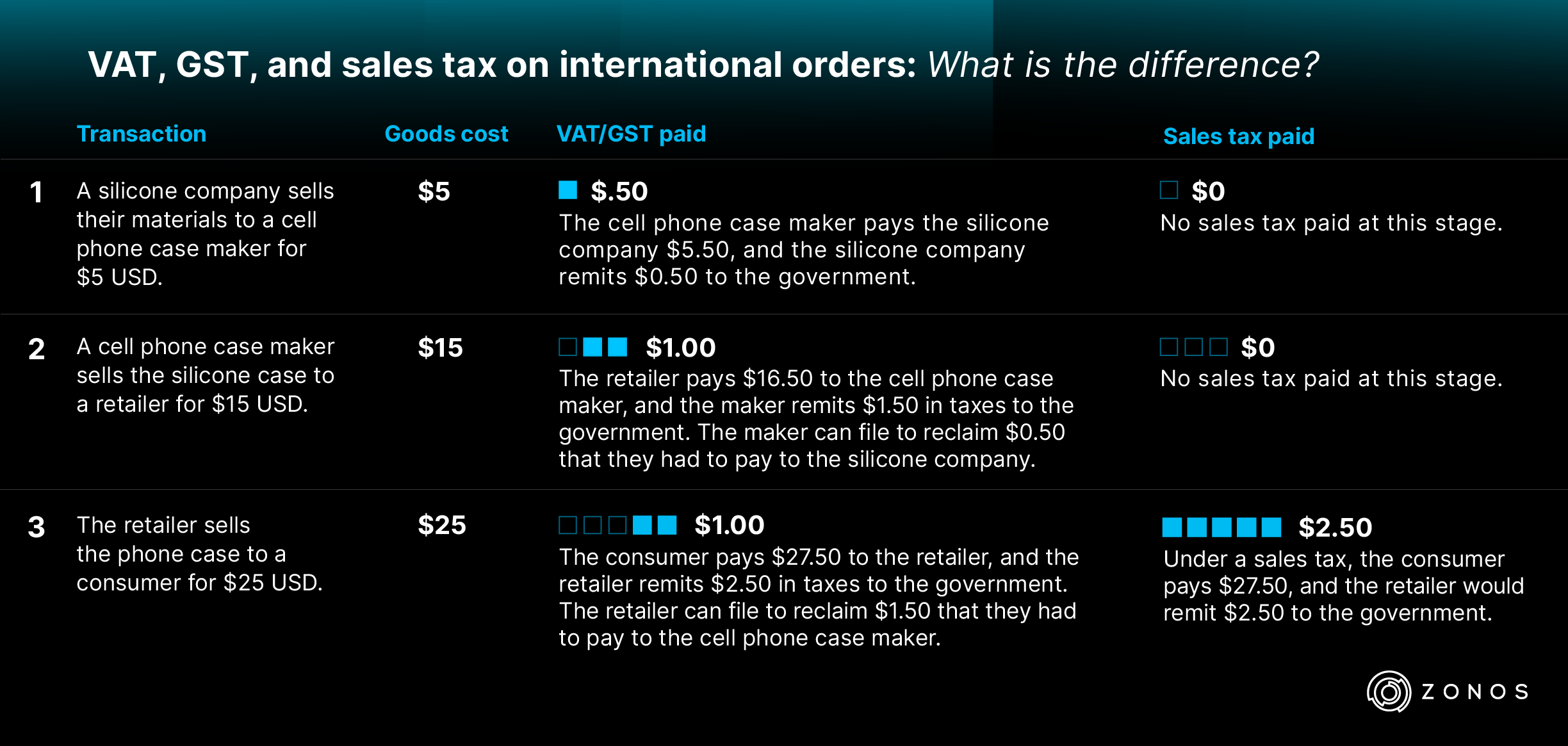

A United Kingdom (UK) bike manufacturer buys bike parts for 50 GBP and incurs a VAT charge of 20% (10 GBP). The bike manufacturer sells the bike to a bike retailer for 100 GBP and incurs a 20% VAT charge (20 GBP). Accordingly, the manufacturer's output tax is 20 GBP and their input tax is 10 GBP, so the manufacturer will pay the difference of 10 GBP to His Majesty's Revenue and Customs (HMRC, the official tax authorities in the UK) and reclaim 10 GBP as reimbursement for the VAT paid when they bought the parts.

The retailer then sells the bike to a consumer for 120 GBP and collects a 20% VAT (24 GBP). The retailer's output tax is 24 GBP and the input tax is 20 GBP. Therefore, the retailer will pay 4 GBP to HMRC and reclaim 20 GBP as reimbursement for the VAT they paid while purchasing the bike from the manufacturer. At every point of purchase, a portion of the tax is remitted to HMRC while the other portion reimburses the seller. The end consumer is the only one who does not get reimbursed.

Taxation history

France was the first country to implement VAT in 1954. Since then, more than 160 countries followed that example and applied some kind of indirect tax—either GST or VAT. Sales tax was first enacted in West Virginia in 1921. There are several reasons why the U.S. is one of the few countries that does not use VAT or GST:

- State rights are an important concept in the U.S., and some states choose not to have any sales tax.

- The state sales tax system is complicated. It is ingrained in every state budget and in every point-of-sale (POS) system. Considering that sales tax rates differ at a local level, it would take time and money to revise and update the budgets and systems.

Tax recap

While VAT, GST, and sales tax are all different methods of taxation, they essentially fulfill the same purpose. Whether a country taxes at a set rate, a percentage based on added value, at the time of consumption, at the time of production and distribution, at the time of sale, or time of import, all these forms of taxation serve the purpose of collecting government revenue.

VAT, GST, and sales tax

Learn how different taxation methods work.Tax is a government levy added to the cost of goods, services, and transactions to generate revenue. Every country has unique and specific rules that govern its taxes. For retailers looking to sell multiple products to multiple countries, the details can quickly get confusing.